KISS Regime Report — Week of 13 July 2026 — Bullish Clear, Cautious Into Tuesday

The verdict holds — records, breadth, and earnings tailwinds all intact. But Tuesday's CPI-and-bank-earnings double header is the real test this rally hasn't faced yet.

═══════════════════════════════════════════

WEEKLY REGIME VERDICT

═══════════════════════════════════════════

BULLISH CLEAR (maintained from last week)

Posture: Full deployment within risk caps · concentrate on the two

confirmed leaders, not the broad tape

───────────────────────────────────────────

THE REASONING

───────────────────────────────────────────

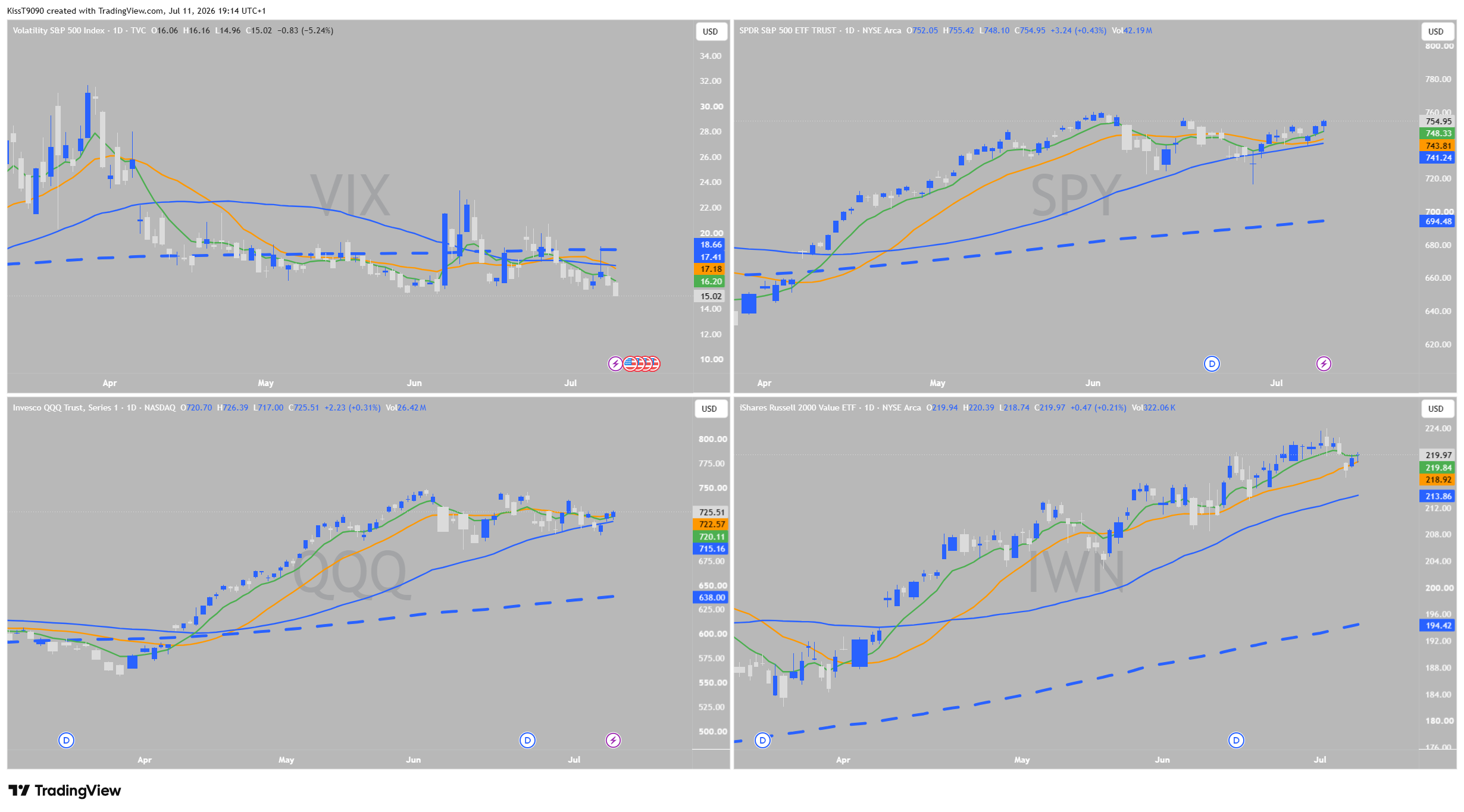

SPY / QQQ / INDEX STATUS

The rally that started two weeks ago on the soft jobs report never broke

stride. The Dow closed above 53,000 for the first time, notching fresh

records through the week. SPY closed Friday at 754.95, VIX fell to 15.02

— genuinely calm, near the low end of its recent range. This is a market

with no fear in it right now.

QQQ told a different story: choppy, range-bound since June, closing

Friday at 725.51. Chip stocks sold off mid-week on profit-taking, then

partly recovered into Friday on SK Hynix’s record-breaking IPO and a

bullish note on Meta’s AI compute business. Net result: tech is roughly

10% off its own recent peak even as the broad index sits at records. That

is the headline nuance for this week — the index is strong, but the

engine that drove it all year has quietly stepped back.

Key levels:

→ SPY: no meaningful resistance overhead — this is price-discovery mode.

First support is the rising 20-day, currently in the low 740s.

→ QQQ: range-bound roughly 700–730 since mid-June. A close outside that

band either direction is the tell.

→ VIX 15 — low and calm. A move back above 20 would be the first crack.

───────────────────────────────────────────

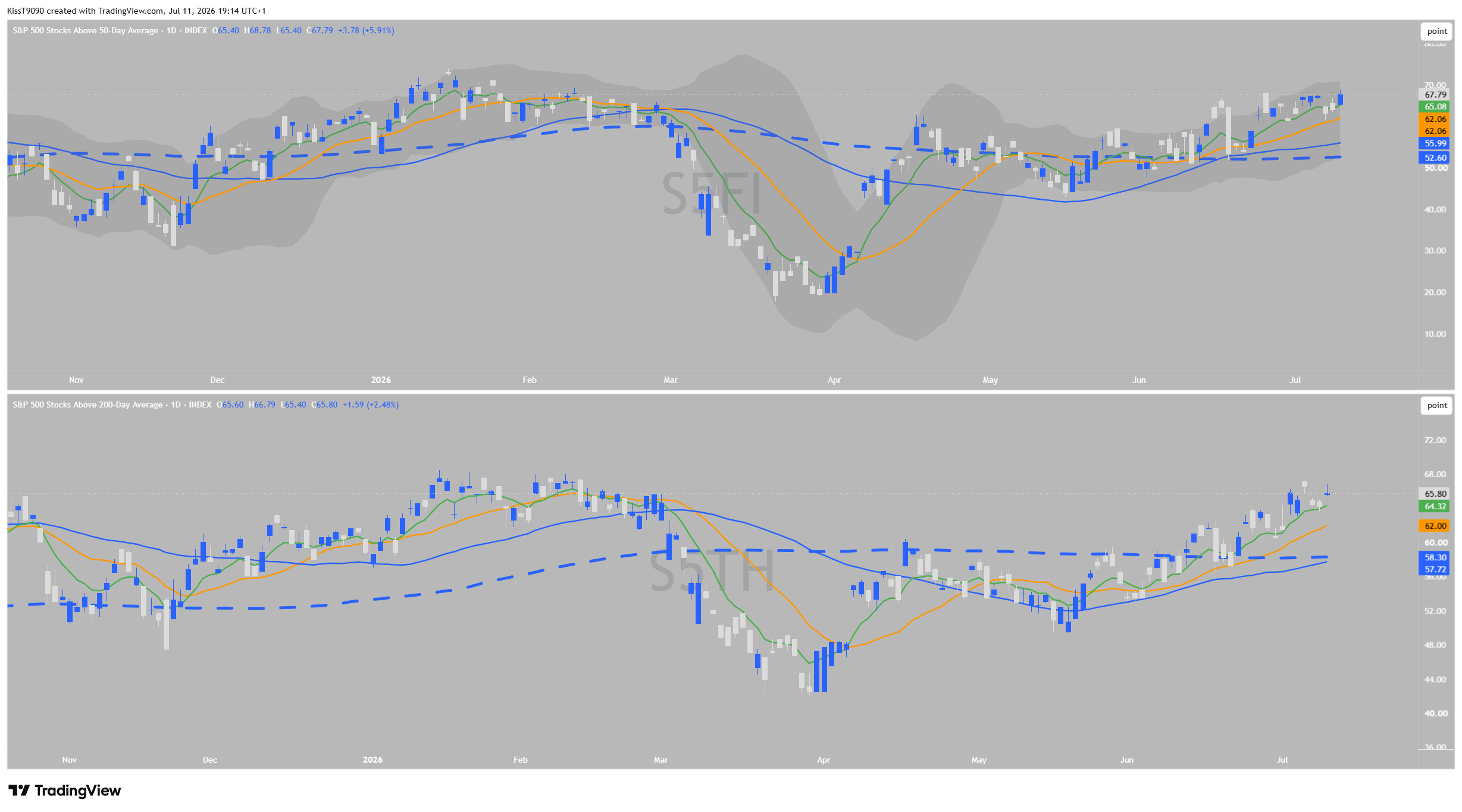

BREADTH CHECK

───────────────────────────────────────────

% of S&P 500 above 50-day: 67.8% (steady, still rising)

% of S&P 500 above 200-day: 65.8% (steady, still rising)

Verdict: STRONG AND STABLE. Both readings are holding at the same high

level as last week — this isn’t a narrow, index-only rally. The average

stock remains participating even as leadership underneath rotates.

───────────────────────────────────────────

WHERE THE LEADERSHIP ACTUALLY IS

───────────────────────────────────────────

This is the real story of the week: leadership NARROWED and SHARPENED.

Two weeks ago nearly every sector was “building leadership” in the

post-jobs-report relief bounce. Now the scanner shows only two names with

genuine, high-confidence trend strength:

→ Health Care (XLV) — RS vs SPY 1.011, trend confidence HIGH, the

strongest slope on the board.

→ Financials (XLF) — RS vs SPY 0.991, trend confidence HIGH, and walking

straight into its own catalyst (below).

Industrials and Utilities are still nominally “building” but on LOW

trend confidence — read those as noise, not signal, until they firm up.

Losing ground, and clearly so: Technology, the Nasdaq 100, Communication

Services, Real Estate, Discretionary, Staples, Materials, Energy, Metals.

That’s a long list — this is a market getting more selective, not less

healthy. New-high indices with narrowing, high-conviction leadership is a

normal and constructive stage of a bull market, not a warning sign by

itself. But it does mean the days of “everything works” are behind us for

now — demand real confirmation, not just a rising tape.

───────────────────────────────────────────

MACRO & CATALYST FLAGS — WEEK AHEAD

───────────────────────────────────────────

This week has a genuine fulcrum day, and it’s not subtle:

→ TUESDAY 14 JULY — the single busiest day of the summer so far:

• 8:30 AM ET: June CPI. May’s print ran hot at 4.2% y/y, the highest

since April 2023, driven largely by Middle East-linked energy prices.

This is the number that decides whether the Fed’s rate-hike risk

(extinguished by the soft jobs report two weeks ago) stays dead or

comes back to life before the July 28-29 FOMC meeting.

• Same day: Citigroup, Wells Fargo, Goldman Sachs, Bank of America and

Morgan Stanley all report Q2 earnings before the bell.

→ WEDNESDAY 15 JULY: JPMorgan reports.

→ Q2 EARNINGS SEASON broadly kicks off this week (Netflix, Johnson &

Johnson, UnitedHealth, United Airlines among others). Aggregate S&P 500

earnings growth is expected near +23% y/y — the fastest pace since

2021. That’s a real fundamental tailwind behind the record highs, not

just sentiment.

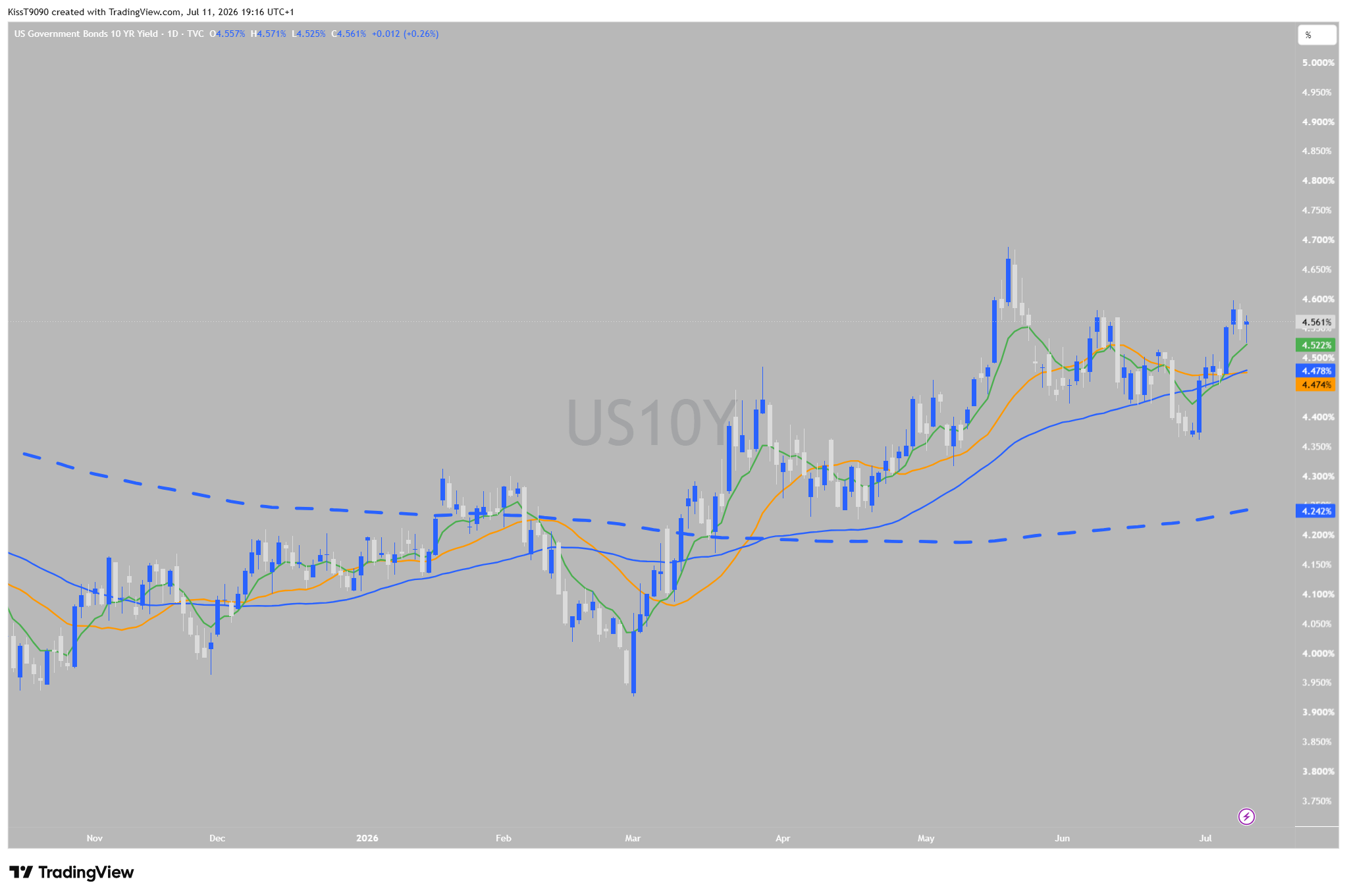

→ Backdrop: US10Y sits at 4.56%, drifting up over the past two weeks but

still well inside its recent range (support ~4.40%, resistance ~4.70%).

Not a red flag yet — but it’s the first place a hot CPI print would

show up.

───────────────────────────────────────────

VERDICT RATIONALE

───────────────────────────────────────────

Nothing here argues for caution: records intact, breadth strong and

stable, VIX low, and a real earnings tailwind arriving this week. Bullish

Clear is maintained, full deployment within caps.

But “clear” doesn’t mean “hunt everywhere.” With leadership down to two

HIGH-confidence sectors, the discipline this week is concentration —

Financials and Health Care carry the conviction; everything else is

increasingly a lower-quality chase, regardless of how the index looks.

And Tuesday is a genuine pivot: a hot CPI print landing on the same day

as five major bank earnings could move the regime fast in either

direction. Trade the plan into Tuesday, not through it blindly.

What would upgrade the picture further: Financials earnings beat cleanly

and the sector’s leadership firms up on the daily, not just the weekly.

What would downgrade it: a hot CPI revives the hike narrative, or a weak

reaction to bank earnings breaks Financials’ structure — either would be

the first real test this rally has faced since the jobs-report relief.

═══════════════════════════════════════════

WATCHLIST + TRADE PLAN (PAID)

═══════════════════════════════════════════

Paid subscribers get the annotated Watchlist and fully-sized Trade Plan

below — this week concentrated in Financials and Health Care, the only

two sectors carrying real conviction into a binary Tuesday. Everything

decided before Monday opens. Upgrade at kisstrading.uk.

───────────────────────────────────────────

Trade Tight · Think in R · Focus on Process

— Radu / KISS Trading

───────────────────────────────────────────

⚠️ Educational only. Not financial advice. Always DYOR.